Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

Why It Pays to Use a 529

Arthur Doglione • May 18, 2017

If you are the proud parent or grandparent of a newborn baby, one of your most important goals is probably to help prepare for college expenses. But what is the best way to do this? While you may have considered … Continue reading

The post Why It Pays to Use a 529 appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

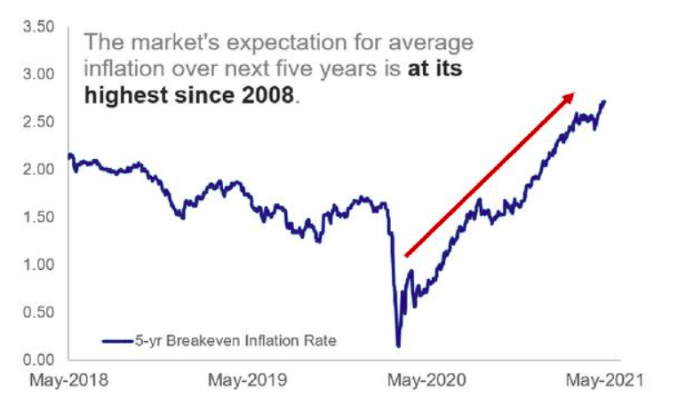

The Market's Expectation for average inflation