Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

Powers of Attorney: A Critical Part of Your Estate Plan

Arthur Doglione • Jan 09, 2020

It is a fact of life that we can’t be everywhere at once. And it is also a sad fact that as we get older, we often lose our capacity to do things for ourselves. Thus, during your lifetime you … Continue reading

The post Powers of Attorney: A Critical Part of Your Estate Plan appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

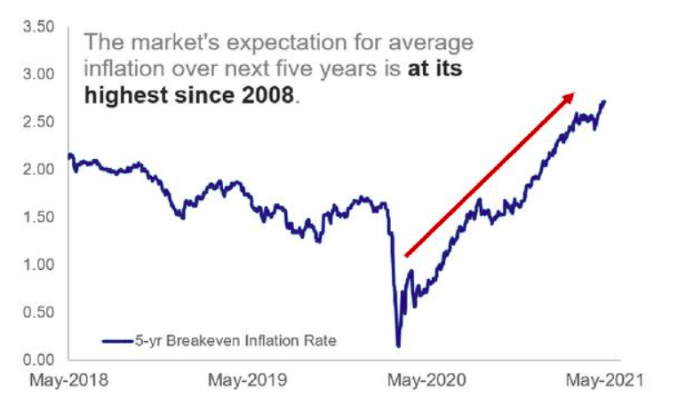

The Market's Expectation for average inflation