Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

So You’re a Trustee. Now what?

Alpha Fiduciary • Feb 23, 2017

It can be a great honor to be named trustee of your family’s or another person’s trust. You may also have named yourself trustee for a trust you funded for the benefit of your heirs because you want to maintain … Continue reading

The post So You’re a Trustee. Now what? appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

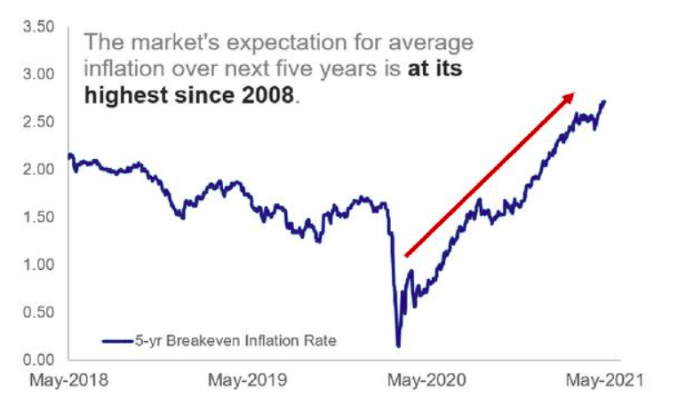

The Market's Expectation for average inflation