Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

To Be or Not to Be…A College Grad?

Arthur Doglione • May 04, 2017

When you consider that Americans owe more than $1 trillion in student loan debt and that the average class of 2016 graduating student held over $37,000 of debt, it begs the question, “Does going to college make financial sense for … Continue reading

The post To Be or Not to Be…A College Grad? appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

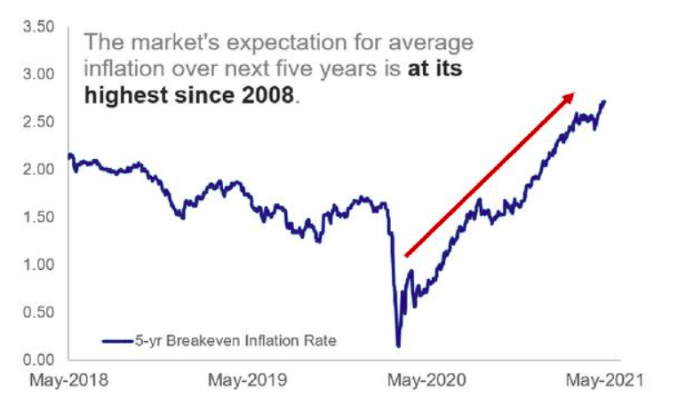

The Market's Expectation for average inflation