2019 Smart Year-End Financial Moves

Arthur Doglione • October 24, 2019

If you’re searching for smart year-end financial moves to make, the following items may help you save money on this year’s taxes or get on track for a better 2020. The below are not in any order of importance, and … Continue reading

The post 2019 Smart Year-End Financial Moves appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

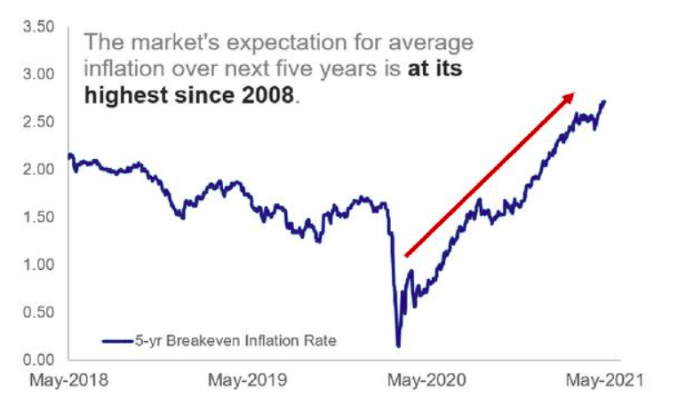

The Market's Expectation for average inflation