Choosing a Trustee is More Than Just Finding Someone You Can Trust

Arthur Doglione • May 21, 2019

You’ve worked hard to create your family trust. You hired a good attorney, funded the trust with your most important assets, and even carefully structured an investment portfolio to consider current and future beneficiaries’ needs. But now who is going … Continue reading

The post Choosing a Trustee is More Than Just Finding Someone You Can Trust appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

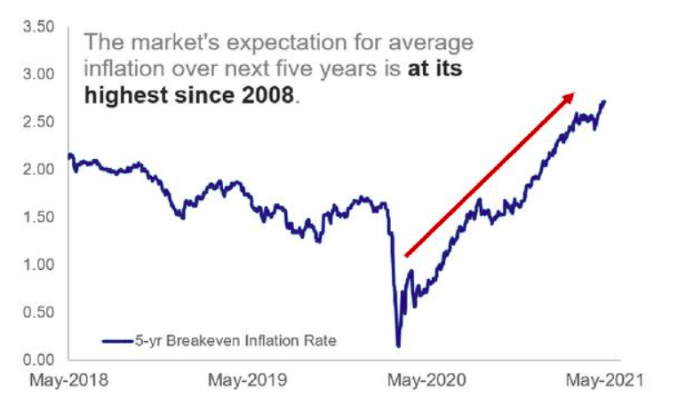

The Market's Expectation for average inflation