Directed Trust versus Delegated Trust: Which one is for You?

Arthur Doglione • November 6, 2019

Now that you’ve decided to establish a trust to preserve your family’s legacy, there are many important decisions to make. For example, will you manage the trust assets yourselves or hire an investment advisor? Will you serve as trustee or … Continue reading

The post Directed Trust versus Delegated Trust: Which one is for You? appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

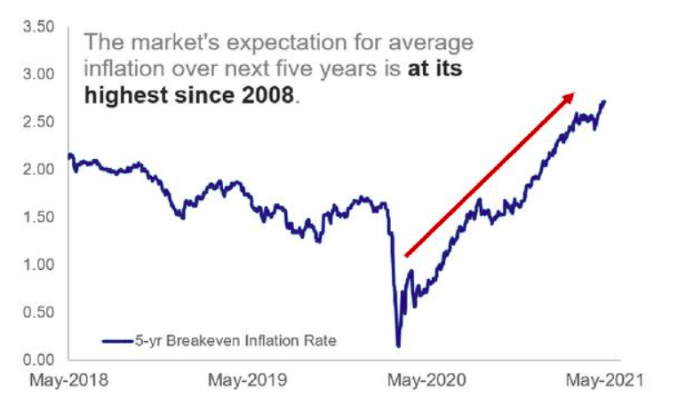

The Market's Expectation for average inflation