Fantastic Estate Transfer Failures and How to Avoid Them

Arthur Doglione • December 10, 2019

What Can We Learn From Famous Estate Transfer Failures? We’ve all heard the names of some of the wealthiest families that built their fortunes from modest beginnings; however, did you realize that few have maintained the same purchasing power … Continue reading

The post Fantastic Estate Transfer Failures and How to Avoid Them appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

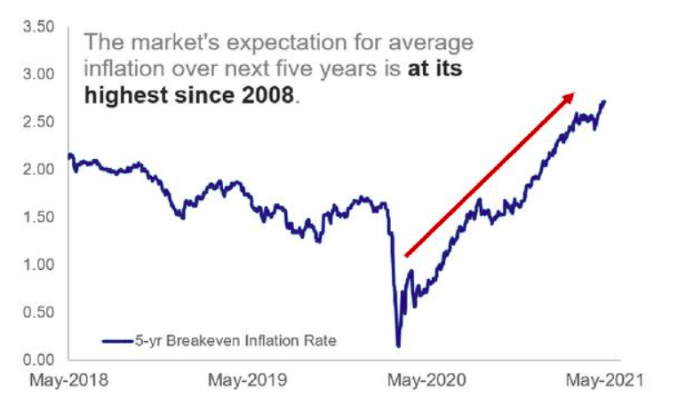

The Market's Expectation for average inflation