Financial Planning Strategies for Today’s Environment

Arthur Doglione • May 6, 2020

If you’re looking for a silver lining in the current market downturn, there are several. We have already written about some timely investment ideas and will continue to present what we think is compelling. But did you realize there may … Continue reading

The post Financial Planning Strategies for Today’s Environment appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

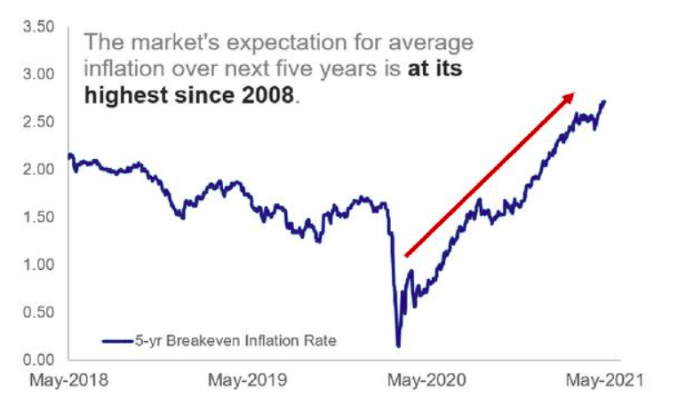

The Market's Expectation for average inflation