How to Avoid Probate Delays and Costs by Making Smart Moves Now

Arthur Doglione • September 25, 2019

Probate can be expensive and tedious. Properly titling assets and taking advantage of beneficiary designations help you avoid probate. Living trusts address more complicated situations. Most people are familiar with the concept of probate and likely recall having been told … Continue reading

The post How to Avoid Probate Delays and Costs by Making Smart Moves Now appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

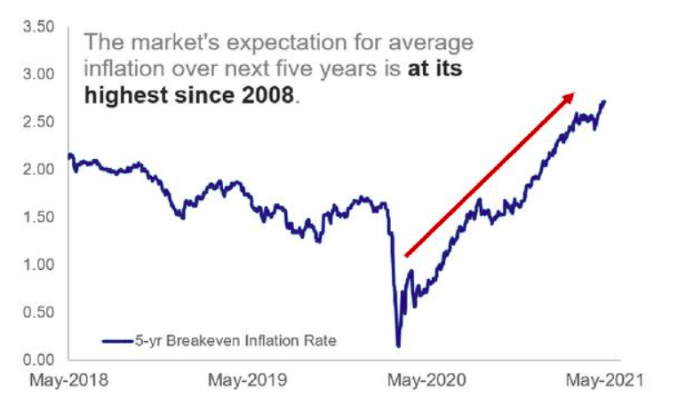

The Market's Expectation for average inflation