How to Respond When Friends or Family Members Want to Borrow Money

Arthur Doglione • March 3, 2020

You’re successful, and your friends and family know it. You never seem worried about money. You have a great job, and you can afford all the basics with ease. Congratulations, you are now a target. As much as you might … Continue reading

The post How to Respond When Friends or Family Members Want to Borrow Money appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

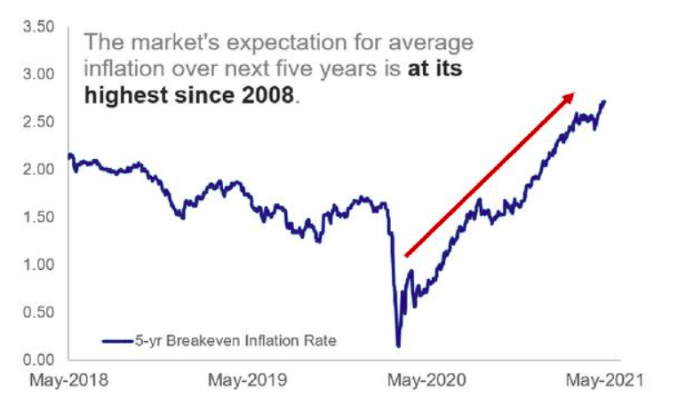

The Market's Expectation for average inflation