Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

Is My Financial Advisor Really a Fiduciary?

Arthur Doglione • Mar 18, 2020

Not all financial professionals must put your interests first When you consult a financial professional about your personal situation, it might be easy to assume that you will receive unbiased financial advice based on your best interests. However, this might … Continue reading

The post Is My Financial Advisor Really a Fiduciary? appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

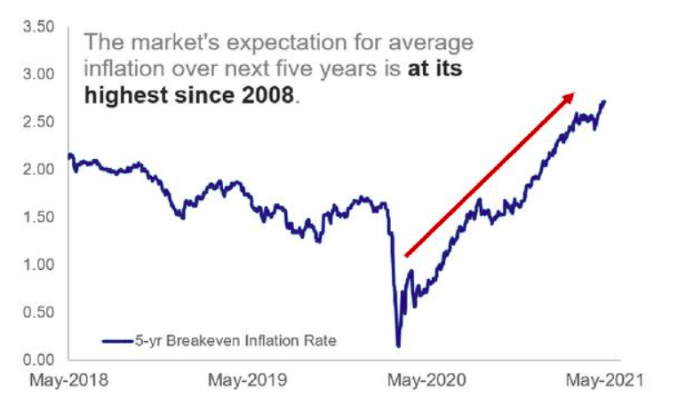

The Market's Expectation for average inflation