Main Street Philanthropy: How the Small Guy Can Give Smart

Arthur Doglione • February 4, 2020

Americans like to give. According to the Giving USA 2018 report, Americans gave over $410 billion dollars to charities in 2017, and 70% of that was from individuals. You read that right: it was people like you and me, not … Continue reading

The post Main Street Philanthropy: How the Small Guy Can Give Smart appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

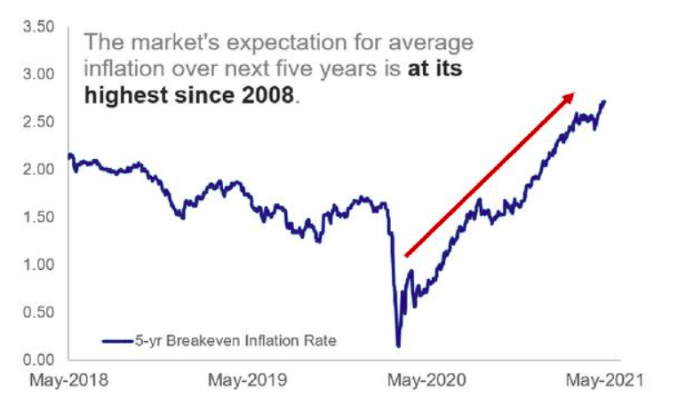

The Market's Expectation for average inflation