Negative Interest Rates and Your Portfolio

Arthur Doglione • May 18, 2020

In the US, we haven’t yet had to experience a significant period of negative nominal interest rates. But given economic fears and the extreme stimulus measures currently underway in Washington, negative rates on US government bonds could soon become a … Continue reading

The post Negative Interest Rates and Your Portfolio appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

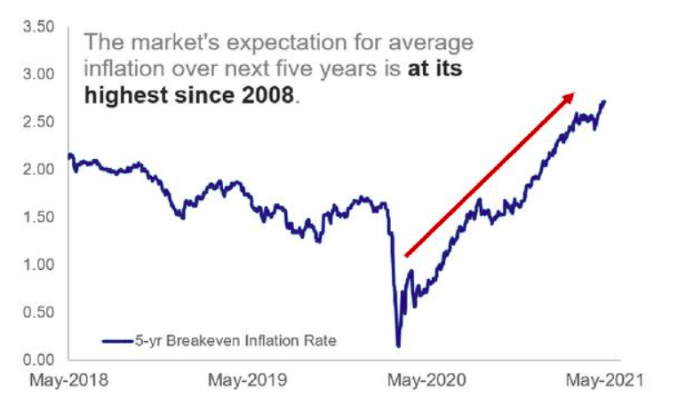

The Market's Expectation for average inflation