Get in touch

555-555-5555

mymail@mailservice.com

480-505-4033

Positioning your Portfolio for Recovery after the Downturn

Arthur Doglione • Mar 30, 2020

It’s easy to forget how high markets had been flying just two quarters ago and how optimistic the mood felt. But thanks to a tiny bug too small to see even with a standard microscope, the world has been turned on its head. Continue reading

The post Positioning your Portfolio for Recovery after the Downturn appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

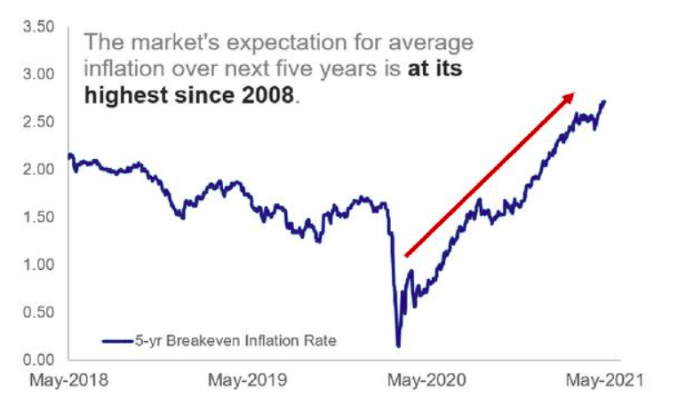

The Market's Expectation for average inflation