Pro Tip – How To Deal With High State Income Tax Rates

Arthur Doglione • June 19, 2020

With the 2018 tax overhaul well behind us, many people who reside in high tax states such as California, Hawaii, New York, etc. are no longer able to fully deduct their high state taxes on their federal tax return. … Continue reading

The post Pro Tip – How To Deal With High State Income Tax Rates appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

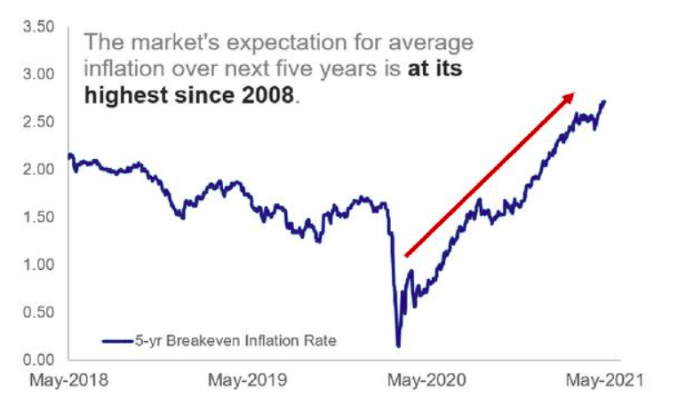

The Market's Expectation for average inflation