What’s Under the Hood of My 401(k)?

Arthur Doglione • June 16, 2017

Not all 401(k)s are created equal. Much like understanding the basic components of the parts under the hood of your car, you should generally be aware of the basic parts of your 401(k) plan to ensure that you know its … Continue reading

The post What’s Under the Hood of My 401(k)? appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

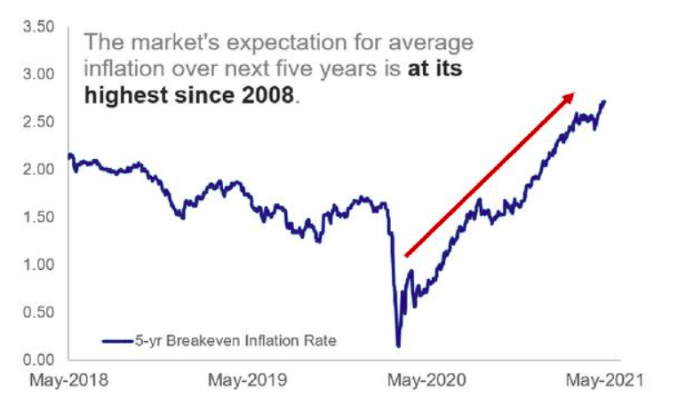

The Market's Expectation for average inflation