Why You Might Want an Intentionally Defective Grantor Trust

Arthur Doglione • November 18, 2019

How an Intentionally Defective Grantor Trust Can Benefit You Usually when we hear the word “defective,” we think about an umbrella that doesn’t open, a dangerous children’s toy, or perhaps our last car. And these are generally never defective by … Continue reading

The post Why You Might Want an Intentionally Defective Grantor Trust appeared first on Alpha Fiduciary.

You might also like

Don't Assume This Cycle Is Like the Last Cycle

Q3 2021, Inflation and Central Bank Policy Are Top of Mind for Investors

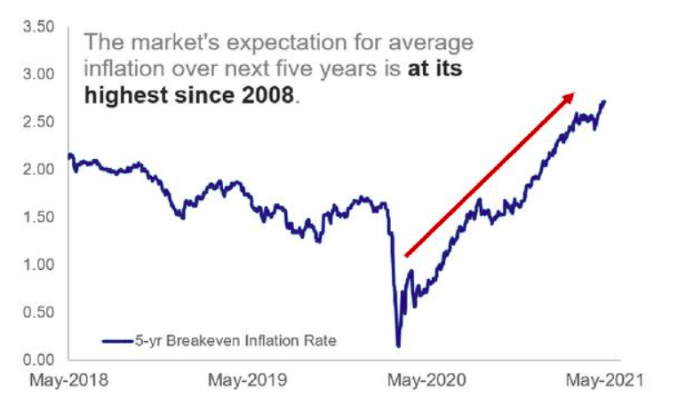

The Market's Expectation for average inflation